Outsell Q2/Q3 Sales Benchmark

Once again, we completed our quarterly benchmark on sales performance in our industry and the outlook for Q3. We’ve been doing this with our partner M3 Learning since the beginning of COVID to provide a bead on the heartbeat of our industry — sales — the blood and oxygen that pump through the business — without which we can’t function.

All I’m about to say is here we go again. In 2022 we emerged from the worst of COVID — the world peeking out from our various cubbies with relief the world was opening up — some sense of ‘normalcy’ on our doorstep. 2023 began with optimism in Q1. Whammo in Q2. Silicon Valley Bank had just failed. First Republic was on the brink, tech seized, inflation and the high cost of debt came home to roost. PE deals ground to a screeching halt. Businesses went into cost cutting and fear mode. 2023 didn’t turn out to be the great year we thought it would be. In fact, it was just weird.

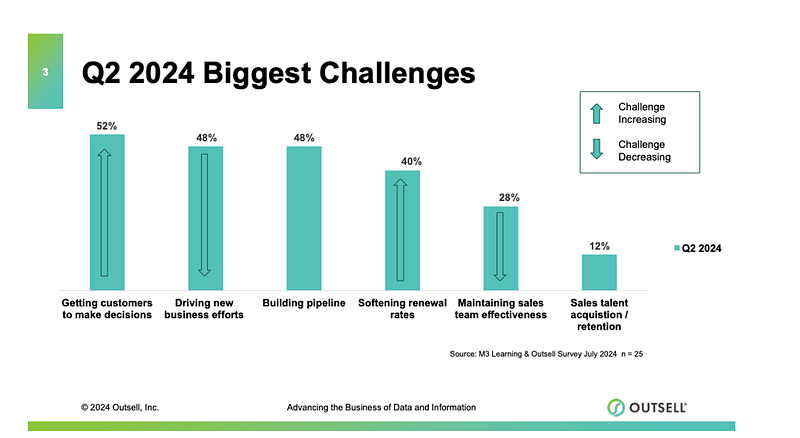

And then Q1 2024 rolled around and with it another sigh of relief. Optimism in Q1. And now sales softening with 52% of respondents off plan by 10% or more and common challenges:

The outlook for Q3 isn’t a lay-up and leaders we serve (CEO/Sales/CRO) are trying to get their head around what is actually going on out there. US GDP is decent at 2.8% announced this week. We’re hearing about general optimism in the UK. Yet, prospect urgency is drifting; more people are involved in decisions. My colleague Christine Rogers CEO of M3 Learning says fewer people want to stick their heads out to assume any kind of risk. There is an accountability malaise.

We are hearing it in M&A too. One I-banker told me deals fell 70% last year and are only up 5% this year — so no real movement off a huge drop in 2023 (PE’s 2008–2009 repeat) Deals are taking longer. The smallest ‘diligence finding or risk’ becomes a mountain — miring time to transaction, if it happens at all. Another accountability malaise.

This week in our Outsell Digital Council Meeting, Christine discussed ways to put energy in a deal and work with both economic owners (exec-level buyers) alongside the user-buyers. She advised how to manage and measure sales teams and SDRs to move things more effectively through the pipe and how to renumerate each. We could have met for a day instead of an hour. We most likely will!

In the meantime, some of this continues to be a factor of our economy and how well it’s doing or isn’t doing. And we’ll be discussing the Economic Outlook right after the Geopolitical Outlook at this year’s upcoming Outsell Signature Event, co-produced with JEGI CLARITY — October 9–10 at the Four Seasons Hotel One Dalton Boston. Request your invitation today. I’ll share more about the program and how it’s coming along. Stay tuned here for ongoing developments. One thing we’ll share for sure is the economic climate that makes sales in our industry go round and round.

A lot of our conversations with clients are focused on the state of the top line. If you’re feeling yours is off — give us a call. You aren’t alone and we can help. Also don’t forget to participate in next quarters benchmark.